Fixed overhead costs are the indirect manufacturing costs that are not expected to change when the volume of activity changes. Some examples of fixed manufacturing overhead include the depreciation, property tax and insurance of the factory buildings and equipment, and the salaries of the manufacturing supervisors and managers. An overhead cost variance is the difference between how much overhead was applied to the production process and how much actual overhead costs were incurred during the period. Therefore, these variances reflect the difference between the Standard Cost of overheads allowed for the actual output achieved and the actual overhead cost incurred. A portion of these fixed manufacturing overhead costs must be allocated to each apron produced.

Fundamentals of Fixed Factory Overhead Variances

The fixed overhead spending variance is a type of variance analysis used to measure the difference between the actual fixed overhead costs incurred by a company and the budgeted or expected fixed overhead costs. This variance provides insights into how effectively a company is managing its fixed overhead expenses in the context of its operations and production activities. An unfavorable fixed overhead budget variance results when the actual amount spent on fixed manufacturing overhead costs exceeds the budgeted amount. The fixed overhead budget variance is also known as the fixed overhead spending variance. The fixed overhead spending variance is the difference between the actual fixed overhead expense incurred and the budgeted fixed overhead expense.

What are two types of overhead cost variances?

An unfavorable variance means that actual fixed overhead expenses were greater than anticipated. This is one of the better cost accounting variances for management to review, since it highlights changes in costs that were not expected to change when the fixed cost budget was formulated. On the other hand, if the budgeted fixed overhead cost is bigger instead, the result will be unfavorable fixed overhead volume variance. This means that the actual production volume is lower than the planned or scheduled production. Let’s assume that in 2023 DenimWorks manufactures (has actual good output of) 5,300 large aprons and 2,600 small aprons.

Managerial Accounting

The other variance computes whether or not actual production was above or below the expected production level. Recall that the standard cost of a product includes not only materials and labor but also variable and fixed overhead. It is likely that the amounts determined for standard overhead costs will differ from what actually occurs. This is a cost that is not directly related to output; it is a general time-related cost. Specifically, fixed overhead variance is defined as the difference between Standard Cost and fixed overhead allowed for the actual output achieved and the actual fixed overhead cost incurred.

- A favorable fixed overhead spending variance arises when the actual fixed overheads incurred by the company are lower than the budgeted fixed overheads.

- The standard variable overhead rate is typically expressed in terms of the number of machine hours or labor hours depending on whether the production process is predominantly carried out manually or by automation.

- In August, the company ABC which is a manufacturing company has produced 950 units of goods in the production.

- The amount of the property tax bill did not depend on the number of units produced or the number of machine hours that the plant operated.

- Therefore, these variances reflect the difference between the Standard Cost of overheads allowed for the actual output achieved and the actual overhead cost incurred.

Financial and Managerial Accounting

In a standard cost system, overhead is applied to the goods based on a standard overhead rate. The standard overhead rate is calculated by dividing budgeted overhead at a given level of production (known as normal capacity) by the level of activity required for that particular level of production. Fixed overhead budget variance is one of the two main components of total fixed overhead variance, the other being fixed overhead volume variance. In this example, the fixed overhead budget variance is positive (2,000 favorable), and the fixed overhead volume variance is negative (-1,040 unfavorable), resulting in an overall positive overhead variance (960 favorable). Fixed overhead spending variance, also known as fixed overhead expenditure variance, measures the difference between actual fixed costs incurred and the budgeted fixed costs. The credit balance on the fixed overhead budget variance account (2,000), has now been split between the work in process inventory account (600) and the cost of goods sold account (1,400) decreasing both accounts by the appropriate amount.

Adverse fixed overhead expenditure variance indicates that higher fixed costs were incurred during the period than planned in the budget. Variable overhead spending variance is essentially the difference between the actual cost of variable production overheads versus what they should have cost given the output during a period. When the actual output exceeds the standard output, it is known as over-recovery of fixed overheads. Initially the actual fixed overhead expense (rent etc) would have been posted to the expense account with the usual entry of debit expense, credit accounts payable (not shown).

To determine the overhead standard cost, companies prepare a flexible budget that gives estimated revenues and costs at varying levels of production. In a standard costing accounting system, the fixed overhead variance is the difference between the standard fixed overhead and the actual fixed overhead. To operate a standard costing system and allocate fixed overhead, the business must first decide on the basis of allocation. Various methods can be used to allocate the fixed overhead including for example, the number of direct labor hours used in production or the number of machine hours used. Fixed Overhead Spending Variance is calculated to illustrate the deviation in fixed production costs during a period from the budget.

If Connie’s Candy only produced at \(90\%\) capacity, for example, they should expect total overhead to be \(\$9,600\) and a standard overhead rate of \(\$5.33\) (rounded). If Connie’s Candy produced \(2,200\) units, they should expect total overhead to be \(\$10,400\) and a standard overhead rate of \(\$4.73\) (rounded). taxes for unmarried couples Two variances are calculated and analyzedwhen evaluating fixed manufacturing overhead. The fixedoverhead spending variance is the difference between actualand budgeted fixed overhead costs. The fixed overheadproduction volume variance is the difference between budgetedand applied fixed overhead costs.

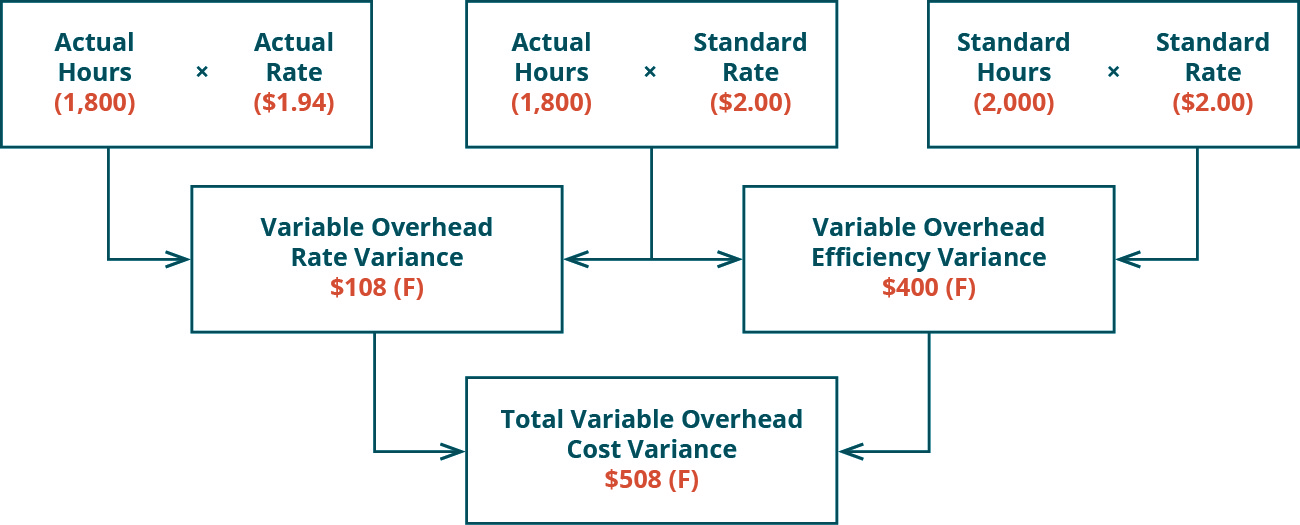

If the outcome is unfavorable (a positive outcome occurs in the calculation), this means the company was less efficient than what it had anticipated for variable overhead. Fixed overheads are a line item in our variance analysis because a fixed overhead is not supposed to vary, as the name suggests. Hence, any significant increase or decrease in fixed cost is a critical point for an entity and shall be dealt with immediately since an unexpected material expense would hurt the company’s financial statements. Variance analysis is the process of identifying and quantifying the differences between actual and budgeted or standard performance measures, such as costs, revenues, or quantities.

ABOUT THE AUTHOR

Mohit Khera, MD, MBA, MPH, is the Professor of Urology and Director of the Laboratory for Andrology Research at the McNair Medical Institute at Baylor College of Medicine. He is also the Medical Director of the Executive Health Program at Baylor. Dr. Khera earned his undergraduate degree at Vanderbilt University. He subsequently earned his Masters in Business Administration and his Masters in Public Health from Boston University. He received his MD from The University of Texas Medical School at San Antonio and completed his residency training in the Scott Department of Urology at Baylor College of Medicine. He then went on to complete a one-year Fellowship in Male Reproductive Medicine and Surgery with Dr. Larry I. Lipshultz, also at Baylor.

Dr. Khera specializes in male infertility, male and female sexual dysfunction, and declining testosterone levels in aging men. Dr. Khera’s research focuses on the efficacy of botulinum toxin type A in treating Peyronie’s disease, as well as genetic and epigenetic studies on post-finasteride syndrome patients and testosterone replacement therapy.

Dr. Khera is a widely published writer. He has co-authored numerous book chapters, including those for the acclaimed Campbell-Walsh Urology textbook, for Clinical Gynecology, and for the fourth edition of Infertility in the Male. He also co-edited the third edition of the popular book Urology and the Primary Care Practitioner. In 2014, he published his second book Recoupling: A Couple’s 4 Step Guide to Greater Intimacy and Better Sex. Dr. Khera has published over 90 articles in scientific journals and has given numerous lectures throughout the world on testosterone replacement therapy and sexual dysfunction. He is a member of the Sexual Medicine Society of North America, the American Urological Association, and the American Medical Association, among others.